- Stablecoin FAQ

- Stablecoin History

- Stablecoin Facts

- What is Stablecoin

Looking to explore Stablecoin? We’ve got answers

With stablecoins, merchants have more questions than answers. That’s where weAudit.com comes in. We’re here to walk with you through this shift, hold your hand through the complexity, and make sure that if you choose to accept stablecoins, you truly understand the pros, the cons, and what you’re really getting into. Along with the real cost of acceptance.

- What is Stablecoin

- A Brief History of Stablecoins

- Fears and Concerns

- Is There Really a Need for Stablecoin — or a Cover Story?

- Monopoly Dynamics

- Custody & Compliance – Why it Matters

- Winners & Losers

- How Government Wins with Stablecoins

- Looking at Stablecoins to Cut Costs?

- Bitcoin vs. Stablecoin: What Merchants Need to Know

What is Stablecoin

A stablecoin is a type of digital currency that’s designed to stay stable in value.

Unlike Bitcoin.org or Ethereum.org, which can swing wildly up and down, a stablecoin is usually tied (“pegged”) to a real-world asset like the U.S. dollar.

Think of it this way:

Bitcoin = gold (volatile, investment-like)

Stablecoin = digital dollar (meant for everyday payments)

With stablecoins, $1 in your digital wallet should always be worth $1. The goal is to give businesses and consumers the speed and efficiency of blockchain payments—instant transfers, 24/7 settlement, global reach—without the rollercoaster of crypto volatility.

A Brief History of Stablecoins

There is no single inventor of the “stablecoin”; the concept evolved through several early experiments, with J.R. Willett’s 2012 proposal for a pegged crypto for his MasterCoin protocol and the 2014 launch of BitUSD on the BitShares blockchain by Dan Larimer and Charles Hoskinson being key early developments. The term “stablecoin” and the first functional stablecoin was then popularized by Tether (USDT), launched in 2014 by Tether Limited.

2014 – The First Stablecoin

The concept began with Tether (USDT), launched as a way to bring “digital dollars” onto blockchain networks. It promised 1 USDT = $1 USD, backed by reserves.

2019 – Expansion

Other issuers entered the space, including TrueUSD and Paxos. This period also saw explosive growth in crypto trading, where stablecoins became the preferred “cash” option for moving in and out of positions without using banks. 2022 – Institutional Attention Circle’s USD Coin (USDC) gained traction, promoted as more transparent and regulated. At the same time, Facebook (later Meta) attempted a global stablecoin project called Libra/Diem, which sparked worldwide regulatory debates—even though it ultimately failed. 2023–2025 – Mainstream Payment Trials Payment giants stepped in. Visa and Mastercard began running settlement pilots using USDC and PYUSD (PayPal’s stablecoin), settling transactions on blockchains like Ethereum, Solana, and Stellar. This marked the first time stablecoins started touching traditional merchant payments. TodayStablecoins represent hundreds of billions in circulation, but their biggest potential shift isn’t replacing Bitcoin or Ethereum—it’s challenging traditional debit rails and becoming part of the hidden backbone of payments.

Fears and Concerns

The digital yuan is programmable and traceable. Authorities can track every transaction in real time. Reports have shown it can be configured to expire if not spent (to boost consumption). Critics warn it could be used to block purchases of disapproved items, or even cut off access for political dissidents.

Nigeria – eNaira

Citizens distrusted it from launch in 2021. To push adoption, Nigeria restricted cash withdrawals from ATMs and banks, essentially forcing people into the CBDC system. Public backlash was fierce; many saw it as an abuse of state power to limit financial freedom.

Ecuador – Dinero Electrónico

The government controlled issuance and management. Citizens rejected it because they feared the state could seize or freeze funds at will. Adoption collapsed and the system was shut down.

Eastern Caribbean – DCash

Not abuse per se, but it showed fragility. The system went offline for two months due to technical issues, leaving people unable to access money. It raised the fear: what happens if a government-controlled digital system just “switches off”?

The Bahamas – Sand Dollar

Not outright abuse, but it centralizes data. Citizens worry it gives the state a complete financial surveillance system, even if marketed as “financial inclusion.”

The pattern is clear:

When governments run digital money, it often tilts toward surveillance, control, and coercion—even if it starts with good intentions. That’s the fear in the U.S. too: stablecoins might begin as “faster ACH,” but without safeguards, they could slide into programmable control mechanisms.

Government Overreach: Private stablecoins could drift toward CBDC-like surveillance if issuers gain freeze/blacklist powers.

Programmable Restrictions: Imagine money that expires if unspent, or can’t be used for certain purchases.

Systemic Risk: An issuer collapse could ripple across commerce.

Consolidation: Small/mid banks get squeezed out, monopolies harden, jobs vanish.

What will the U.S. do with all this power?

Is There Really a Need for Stablecoin — or a Cover Story?

ACH already works.

Same-Day ACH and FedNow cover most domestic cases cheaply and quickly. For everyday B2B and B2C flows, there’s no burning hole only stablecoins can fill.

Where stablecoins really shine:

Cross-border transactions.

Programmable conditions (escrow, milestone-based payouts, instant splits).

24/7 availability for industries that can’t wait for banking hours.

So what’s the bigger play?

Roll it out as “innovation,” eliminate smaller players, gain share, then ratchet up the tolls once alternatives are weakened. The story is speed and global reach. The outcome could be fewer rails and higher fees later.

Monopoly Dynamics

Stablecoins won’t topple Visa and Mastercard. They’ll strengthen them.

- Licensing rules ensure only well-capitalized issuers (megabanks) can play.

- Networks (Visa/Mastercard) integrate stablecoin settlement inside their ecosystems, guaranteeing they still clip the ticket.

- Big banks will make money by charging to hold the reserves behind stablecoins and by running the compliance checks — services only profitable at their scale.

- Wallet dominance (Apple, PayPal, big-bank wallets) means the distribution channel itself is controlled.

The outcome?

A vertically integrated stack where issuers, wallets, networks, and custodians are the same giants — with fewer competitors and higher switching costs.

Custody & Compliance – Why it Matters

Custody

- Stablecoins have to be backed by reserves (cash, T-bills).

- Somebody has to hold those reserves safely, prove they exist, and manage redemptions.

- That “somebody” is usually a bank or large financial institution.

- The service isn’t free: they’ll charge custody fees to stablecoin issuers.

- Only big banks with scale can do this cheaply and at the level regulators demand. Small banks get priced out.

Compliance

- Every stablecoin transaction must follow KYC/AML rules (Know Your Customer / Anti-Money Laundering).

- This means monitoring wallets, screening transactions, filing reports.

- That infrastructure is expensive to build, but once you have it, you can “rent it out” to issuers.

- Again, only giant players like JPMorgan, Citi, Visa, Mastercard, and PayPal can build compliance engines at global scale.

Winners & Losers

Winners:

- Mega-banks and card networks. They will co-opt the rails, as Visa and Mastercard already are, and re-monetize them through custody fees, spreads, and compliance packages.

- Global merchants and platforms. Cross-border payments get simpler and faster — if they don’t give back savings through hidden fees.

- Fintech wallets/gateways. New products and services built on programmable money rails.

- Government and regulators. Gain greater visibility into transactions, tighter control over the financial system without needing a direct CBDC, and extend U.S. dollar dominance globally.

Losers:

- Community and mid-size banks. Debit interchange and ACH settlement are lifelines. Stablecoins bypass them, meaning deposits migrate, fee income disappears, and consolidation accelerates. Thousands of jobs in operations and regional banking could vanish.

- Regional processors and boutique acquirers. Margins shrink as rails collapse into fewer, bigger hands.

- Consumers. Lose perks and protections. Chargebacks, fraud monitoring, and liability limits are not built into most stablecoin systems. If a transaction goes wrong, the consumer may be out of luck. Confusion and mistrust. For many, “crypto” still equals risk. A push toward stablecoins could spook average consumers, slowing adoption. Less float. With credit cards, you buy now and pay later. With stablecoins, money leaves your wallet instantly — no time buffer.

How Government Wins with Stablecoins

Visibility & Surveillance

- Every transaction can be monitored in real time.

- Tax compliance becomes easier; under-the-table commerce shrinks.

- Law enforcement gains a powerful tool to track money flows.

Policy Leverage

- If stablecoins become mainstream, regulators can set the rules of the rail.

- This means the government doesn’t have to issue a CBDC directly — they can control private stablecoins through licensing and reserve requirements.

Geopolitical Power

- Stablecoins pegged to the U.S. dollar extend dollar dominance globally.

- The U.S. can project financial influence abroad without launching an official digital dollar.

Revenue & Control

- More reporting = more taxable activity captured./li>

- More consolidation = easier oversight, but also fewer banks to regulate (convenient for regulators).

Looking at Stablecoins to Cut Costs?

Many merchants explore stablecoins because they’ve heard they can process payments faster and cheaper.

Unfortunately stablecoins are real and already being used. However, they’re mostly limited today to crypto traders, cross-border payments, and a handful of big tech pilo

The good news, you don’t need to wait for stablecoins to lower your costs. At weAudit.com, we’ve been saving companies 30–40% on their credit card processing fees for years — without changing your processor and without gambling on unproven technology.

Our audits uncover the hidden markups, padded fees, and “junk charges” that processors slip into your statements. Then we make sure your business pays the absolute minimum the law allows.

And when stablecoins do become widely available to merchants, we’ll be right there to hold our clients’ hands — making sure they adopt this new technology at the absolute lowest cost and implement it in the most cost-effective way possible.

Stablecoins may be the future, but your savings can start today.

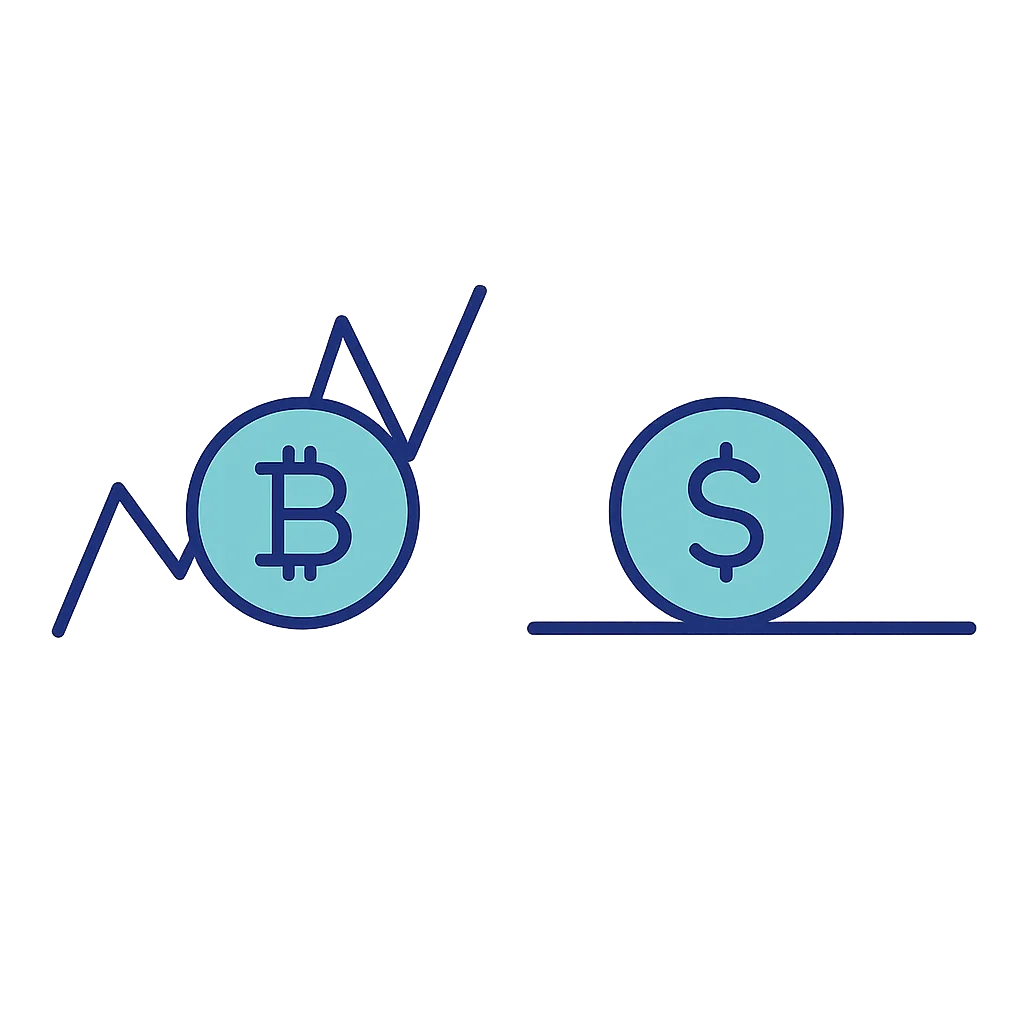

Bitcoin vs. Stablecoin: What Merchants Need to Know

Bitcoin: Digital Gold

- Volatile asset. Bitcoin’s value swings daily, sometimes by double digits.

- Store of value. Often compared to gold — a hedge, not a payment rail.

- Speculative. Consumers and investors hold it hoping the price will rise, not to settle invoices.

- Slow & costly. Transaction throughput is limited, and fees can spike in busy times.

Stablecoins: Digital Dollars

- Pegged to fiat. Usually tied 1:1 to the U.S. dollar (USDT, USDC, PYUSD).

- Designed for payments. Fast settlement, programmable features, and lower volatility. Note, there is volatility

- Backed by reserves. Ideally held in cash or Treasuries, though quality varies.

- Growing rails. Visa, Mastercard, and PayPal are piloting them — they’re aiming for merchant use, not speculation.

The Key Difference

- Bitcoin is an investment.

- Stablecoin is a payment instrument.

- Third bullet point

Think you don’t need an audit?

Take our audit challenge to see if you can find the $79,551 in overbillings.

How Easy It Is

How Easy It Is

It’s never been so easy to save money!

Step 1

Upload your statements

Step 2

We complete a 10 point, comprehensive audit on your statements

Step 3

We review your free audit results with you. Enjoy the savings.

A Few of Our Numbers

About weAudit

weAudit.com, Founded in 2009 by Robert Day, is America’s #1 Credit Card Processing Auditing Firm. The firm specializes in all aspects of credit card processing fees, interchange management, fraud, PCI Compliance, and surcharging, aiming to save businesses money and provide ethical, transparent, and secure services. In 2019, they were awarded the Better Business Bureau’s Torch Award for ethics and community service. weAudit.com is dedicated to making a positive impact by supporting various charitable organizations and upholding high standards of respect and privacy for their clients.

Want to talk?

- Call us today 800-672-1292

- Book a free consultation

As seen on