Warning If You Use Bank of America For Credit Card Processing

Read More

Read More Check out our other insights here

If credit card processing networks controlled ACH Fees, then ACH fees would look very different than they do today.

When addressing the Senate back in 2011, Senator Dick Durbin said, “Credit Card Interchange is a price fixing scheme.”

Finally someone, besides me, that sees this for what it is.

If credit card processing networks controlled ACH Fees, it would look something like this:

I could go on and on, but I think you get the idea.

There are things most merchants don’t realize about credit card interchange. Like when a retail merchant has to key a transaction and puts in the wrong billing zip code, Visa hits that merchant with a substantially higher interchange fee. Why? Because this transaction is considered a higher risk. This makes sense, except for one major thing… WHO is at higher risk? It’s the merchant will not get paid if the transaction turns out to be fraudulent in addition to being out the cost of the product or service they provided.

Let’s make this simpler to comprehend… Imagine your child just turned 16 and started driving. The insurance company tells you that your rates are going way up. Of course that makes sense now that you have a high risk driver. Imagine if they end up getting into an accident and the insurance company tells you, “sorry, but your child is not covered” even though your rates soared to offset the risk. In no other industry would this be acceptable.

Or, how about paying much higher interchange fees because a transaction is tax exempt? Why would you have to pay way higher interchange fees just because the buyer had a tax exempt status?

Again, I could go on and on, but I hope you get the idea. They make up crazy rules in order to force merchants’ transactions to downgrade so they can charge them a higher interchange fee.

In order to keep merchants guessing, they are constantly adding and removing fees, as well as adding hundreds of new interchange fees since as far back as 1991. At that time there were a total of only eight interchange categories, and it grew to just over three hundred by 2009. Today in 2024 there are approximately one thousand! Why are there so many interchange categories?? Well, because they can!

One of our greatest expenses is updating our software just to keep up. Every April and October they change the rates; however, unlike what the media says, (see below) the rates hardly ever move.

In the chart above you will see in 2009 the highest rates ranged between 2.95% – 3.25%. As of today (September 2024) fifteen years later, the highest tiers range between 3.15% and 3.30%. That’s about 0.01 per year. Nothing else has had that small of an increase that I know of, and as we all know, most things have skyrocketed over the last few years.

So why would they say credit card fees keep going up?

Read some of the other insights like:

The common theme is credit card processors add in made-up fees, inflated fees etc.

Here is the good news! We help merchants with Interchange Optimization™ – getting merchants transactions to settle at the lowest interchange rates, reducing the average merchant’s interchange fees as much as 30-40%.

Credit card processors do everything they can to make things hard and make merchants pay higher fees. We do everything we can to help merchants get their credit card fees reduced, and for pennies on the dollar. Make sure you check out our fees at the bottom of our home page.

Then you will see why Kevin Harrington from Shark Tank says we truly are a NO-BRAINER!

Subscribe to insights – Read more Insights – Submit an article idea

Read More Check out our other insights here

Is the title a statement or a question? It’s up to you to decide. But let’s shed some light on this, and maybe it’ll help you make up your mind.

I discuss this kind of statement in my latest book, The Great American Heist – How Credit Card Processors Steal Businesses’ Profits. In Chapter 13, titled “Different Billing Types: Zero Disclosure/Numeric Billing,” I cover how credit card processors often use hidden codes to represent interchange categories, instead of using the already complex official interchange categories.

To clarify, while interchange categories are complicated, they can still be understood with enough time and expertise. For instance, “EIRF” stands for Electronic Interchange Reimbursement Fee, a term that might mean little to the average merchant. However, with some research, you can learn that it often indicates a missing or incorrect zip code, depending on your Merchant Category Code (MCC). Yes, it’s confusing—and that’s exactly how the issuing banks and processing networks want it.

Below is an example of how your interchange fees should be displayed. If your statement looks like this, we can review each line item and explain why a transaction was downgraded. A downgrade means the transaction settled or cleared at a higher interchange rate. We can also determine whether your credit card processor charged you the actual interchange fees or if they inflated them. Now, before we get too far, you might be thinking, “Of course they’re charging the right amount.” But what many don’t realize is that merchant processing isn’t regulated. Credit card processors can inflate or even invent fees. For more on this, see, “How Can I Have the Lowest Discount Rate and the Worst Deal?”

Interchange fees make up about 90% of your total processing costs. So controlling your interchange fees is the most important step to controlling—or reducing—your overall processing costs. Part of that involves ensuring that each transaction clears at the lowest possible rate. But to do that, you first need to understand how the transaction settled and where it might have gone wrong.

Below is how your interchange should be disclosed. If your statement includes this information, we can tell you whether your transactions are settling at the best possible interchange fees or if there are settlement issues.

We can also determine if your credit card processor is inflating your interchange fees. For more information, check out an article I wrote for Forbes on this exact issue.

Now, let’s take a look at a Chase Paymentech statement below.

Instead of providing the actual interchange category, such as “MC-BUS LEVEL 3 DATA RATE I,” they use a code like “V148.”

Did the transactions clear at the lowest interchange rate or the highest? If you don’t know, how can you improve it? Are they inflating the interchange fees? This is a question I explore further in the Forbes article.

Why are they hiding the interchange categories? Generally, things are hidden when someone doesn’t want you to see something. Could it be that they’re inflating or padding the interchange fees? Take a close look at the image below—a Chase Paymentech statement where two of the largest credit card processors settled for $52 million after being accused of inflating interchange fees. Even after the settlement, they maintained they did nothing wrong and stated they would continue conducting business as they had been.

I wish I could say, “Call us, and we’ll make Chase Paymentech transparent,” but unfortunately, that’s not possible. They’d rather lose merchants than reveal their secret coding system.

Merchant processing is not regulated, which means any processor you deal with can hide fees, inflate them, or even add made-up charges. If you’re like most merchants, you’ve probably switched credit card processors a few times, only to find yourself facing the same situation—being taken advantage of again.

This is why some of the largest companies in the world turn to us for help in navigating this highly complex part of their business. On average, our clients pay 40% less in fees after they start working with us. To be clear, we don’t sell credit card processing. We audit credit card processors, negotiate, and vet agreements. Our guarantee is simple: if you find a company that saves you more money after hiring us, we’ll refund you double what you’ve paid us over the last six months. Plus, everything we do is backed by a Love-The-Results-Or-Don’t-Pay Guarantee.

This is why Kevin Harrington from Shark Tank says we truly are a NO-BRAINER!

And why Trevor Gleason, Treasurer of Facebook UK, called us “a company not to be overlooked.”

Get Your Free Audit Schedule A Free Consultation

Subscribe to insights – Read more Insights – Submit an article idea

Read More Check out our other insights here

Read More Check out our other insights here

Read More Check out our other insights here

Read More Check out our other insights here

Read More Check out our other insights here

Read More Check out our other insights here

Read More Check out our other insights here

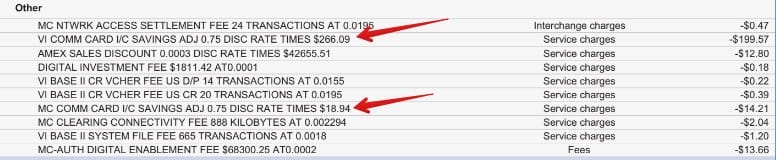

Credit card companies make it difficult for credit card transactions to settle at the lowest interchange fees by adding stringent rules. However, they came up with a solution to fix this for you called I/C (Interchange Clearing) Fee, or another processor calls it CCIS (Commercial Card Interchange Service). It is when the credit card processors fix the transaction for 75% of the savings.

See below for what it looks like on your statement.

Before you think this is a good deal, let’s do the math and shine the light on this a little more…

If a merchant runs a $500 transaction that was going to downgrade from missing data, they will insert the missing data before sending it off to the processing networks. By doing this, the transaction will settle at a lower interchange fee – on average, about 85 basis points less, saving the merchant $4.25. The processor will take $3.19 and give the merchant $1.06 and say the merchant should be happy. After all, if not for them, they would have lost $4.25.

However, third-party companies will also do this and their fee is only 5 basis points. So, let’s do the math on that: .05% of $500 is only $0.25, so the third party will save you the same $4.25 and they will take $0.25 and give you the $4.00.

Option A – Use your processor who is creating the problem to fix the problem and you keep $1.06.

Option B – Use a third party that helps fix your interchange and you keep $4.00.

I think it is an easy decision. The only exception is when your ERP or POS blocks third parties to increase profits and prevent you from getting help.

Click here to schedule a call to learn how easy it is to fix this.

Subscribe to insights – Read more Insights – Submit an article idea

Read More Check out our other insights here